THIS MATERIAL IS A MARKETING COMMUNICATION.

ESG Sector Review: Metals and Mining

In the world of Environmental, Social and Governance (ESG), the Metals and Mining sector is a sector that is increasingly facing scrutiny from investors and regulators. This is because the business activities of Metals and Mining companies inherently bring about disruptions to the natural environment. Whilst this may be true, it does not necessarily mean the ESG outlook for the sector is bound to go downhill.

In fact, the continuous development of green technologies, such as electric vehicles (EV) and hydrogen fuel cells, will create new demand for various metals. Therefore, we expect the sector to encounter both risks and opportunities under the prevailing trend of ESG.

In this article we discuss ESG considerations that come at play for the Metals and Mining sector now and in the future.

The ESG Context

Inherent environmental externalities but enablers of decarbonisation

Mining, by nature, has negative impacts on the environment due to its extraction of natural resources. For example, steel is made from iron that is extracted from rocks and minerals, then produced in basic oxygen furnaces or electric arc furnaces. 1 Copper is extracted from its ore underground or by open pits, and refined using electrolysis. 2

Significant amounts of greenhouse gas emissions as well as sulphur dioxide is generated through power generation for mining operations, and as a product of refining metals. Bulk metals such as steel and thermal coal generate a lot of carbon emissions for production whereas precious metals such as gold and platinum generate relatively lower carbon emissions to produce. 3 Notwithstanding such inherent environmental externalities, metals are crucial raw materials for technologies that facilitate the transition to a ‘green’ economy. We discuss in more detail how metals are key enablers of decarbonisation in later sections.

As mining companies expand their business operations, their operational emissions also increase inevitably. As such, mining companies actively explore avenues to innovate and reduce emissions in tandem to growing their business. For instance, despite Hindalco’s energy consumption needs are mostly met by fossil fuels, renewable energy consumption increased by 2200% over the past 3 years. Hindalco installed and commissioned solar and hydro power plants at its mines as well as entered third-party purchase agreements since 2018. 4 Hindalco’s subsidiary Novelis also undertook a pilot project to collect used beverage cans for recycling using state-of-the-art technology at their plant in Korea to produce aluminium sheets.5

“Metals and Mining sector leaders are heading for long-term ESG targets. We expect them to continuously strive in environment protection, bear social responsibilities and improve on corporate governance to achieve business sustainability.”

-Bingyao Chen, Investment Analyst (Mirae Asset)

Pioneering technologies and regulations also play a part in the decarbonisation of the Metals and Mining sector. For example, the use of hydrogen as energy fuels as well as the use of carbon capture technologies in steel production are advanced ways to reduce emissions in the mining and refining process. Policies such as Mainland China’s steel capacity swap and production curbs are also ways to control the environmental performance of the sector. 6

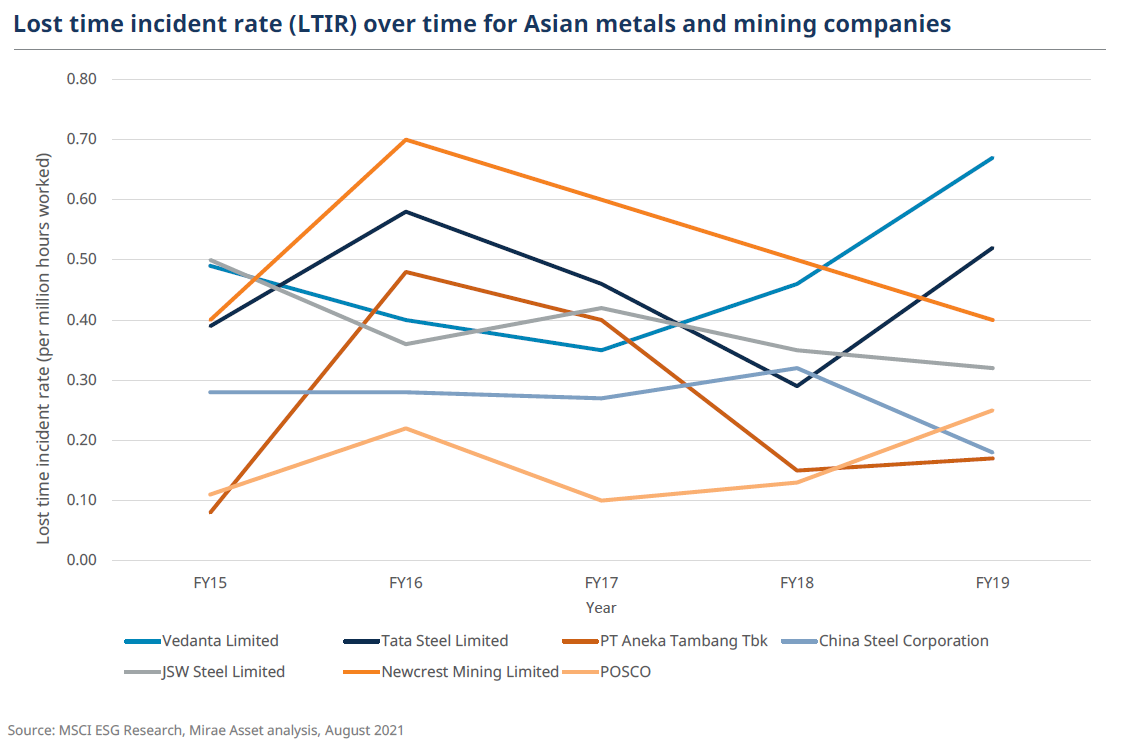

Safety considerations within and outside of mining companies

Metals and Mining is labour-intensive and is susceptible to fatalities and injuries due to hazards like powered haulage and machinery. Poor safety records may result in regulatory compliance costs, reputational risks, and even operational downtime.

In order to support the implementation of safe steel mills, POSCO recently promoted a ‘Smart Safety’ initiative that introduces cutting-edge technologies such as artificial intelligence, smart wearable devices, and automated robots to build a disaster-free working environment. For example, robots are utilised to replace high risk manual work like those at high temperatures or heights. Another example is the Smart Safety Ball, the word’s first technology developed by POSCO, which detects the presence of harmful gas when thrown into an enclosed workspace prior to workers’ entry.7

Mining facilities are often active over long periods of time; the rights and accessibility of surrounding communities may be affected through the environmental and social impacts of mining operations. In light of these considerations, mining companies rely on good relations with local communities for their social license to operate. Mining companies generate indirect economic value through creating local employment opportunities. For example, Tata Steels employed more than 31,000 permanent employees in 2020 and placed local sourcing of labour as an emphasis area for the company.8 Outside of its core business activities, Tata Steel also held various other initiatives to create economic opportunities, such as collaborations with Zomato and Swiggy for online vegetable selling which disbursed ₹7.32 lakh income to date, supporting 203 farmers.9

The ESG Road Ahead

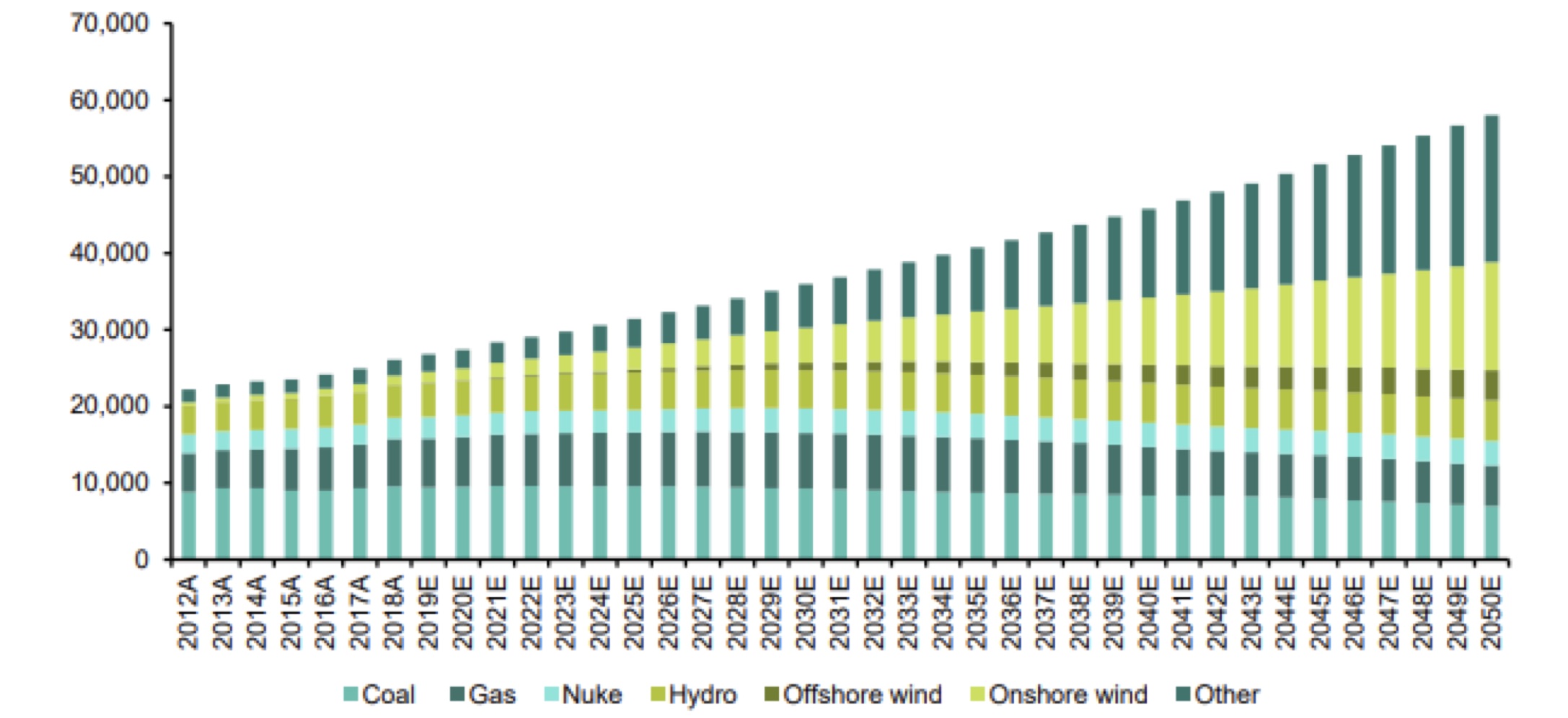

It goes without saying that thermal coal hinders sustainable development and is receiving negative sentiments from governments and investors alike. Projections of global power output indicate that coal will fall by 11% by 2040 – a rate of decline that is far from satisfactory in the world’s trajectory to net zero (a state in which the greenhouse gases going into the atmosphere are balanced by removal out of the atmosphere). 10 Nonetheless the global phase out of coal will likely have negative implications on the Metals and Mining sector; companies will need to re-adjust their business strategies to reduce or remove thermal coal exposure.

Projection of global power output by 2050

Source: Bernstein Research, May 2021

Carbon pricing is a key approach that facilitates the global transition to a low carbon economy, through using market mechanisms to pass the cost of emitting greenhouse gas emissions on to emitters. China, having launched pilot carbon trading schemes has launched a national one for the power industry. The scheme will cover cement and aluminium by 2022, and steel, paper and petrochemicals and other industries by 2025.11 Chinese Metals and Mining companies will therefore need to prepare accordingly for carbon pricing in the coming years.

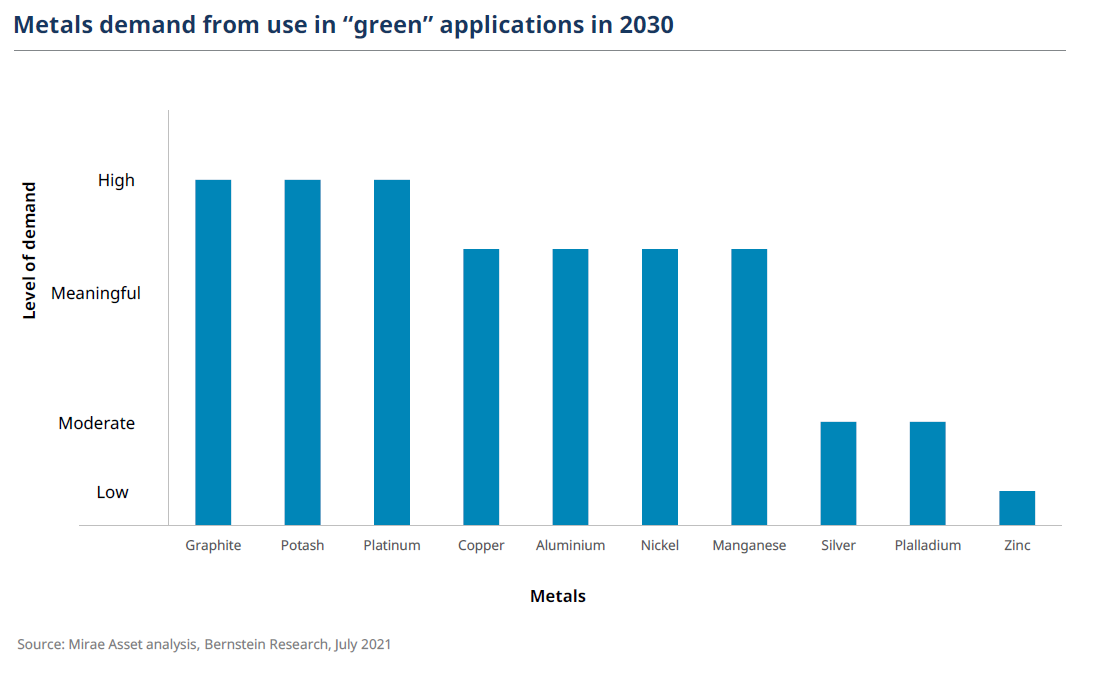

Looking ahead and as discussed in earlier sections, there are certainly opportunities for the Metals and Mining sector in a “green” economy, driven by demand for “green” applications. Metals are key enablers for the development of a hydrogen economy, especially platinum in the manufacturing of fuel cells and production of green hydrogen, and the widespread of EV adoption. Furthermore, aluminium and copper are also crucial raw materials for building out green electricity generating infrastructure like on- and off- shore wind power systems. Aluminium is also an ideal substitute for steel in vehicles because of its light weight hence reducing energy required to push the vehicle.12

1 ThermoFisher Scientific, Accessed July 2021

2 European Copper Institute’s Copper Alliance, Accessed July 2021

3 Bernstein Research, May 2021

4 Hindalco Sustainability Report FY 2019-20, August 2020

5 Hindalco Sustainability Report FY 2019-20, August 2020

6 Macquarie Research, April 2021

7 POSCO Corporate Citizenship Report 2020

8 Tata Steel Integrated Report & Annual Accounts 2020-21

9 Tata Steel Integrated Report & Annual Accounts 2020-21

10 Bernstein Research, May 2021

11 Macquarie Research, April 2021

12 Bernstein Research, May 2021

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KIIDs”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KIIDs can be obtained from www.am.miraeasset.eu/fund-literature . The Prospectus is available in English, French, German, and Danish, while the KIIDs are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KIID before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Australia: The information contained in this document is provided by Mirae Asset Global Investments (HK) Limited (“MAGIHK”), which is exempted from the requirement to hold an Australian financial services license under the Corporations Act 2001 (Cth) (Corporations Act) pursuant to ASIC Class Order 03/1103 (Class Order) in respect of the financial services it provides to wholesale clients (as defined in the Corporations Act) in Australia. MAGIHK is regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws, which differ from Australian laws. Pursuant to the Class Order, this document and any information regarding MAGIHK and its products is strictly provided to and intended for Australian wholesale clients only. The contents of this document is prepared by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Australian Investments & Securities Commission.

Copyright 2021. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.